Join day by day information updates from CleanTechnica on e-mail. Or observe us on Google Information!

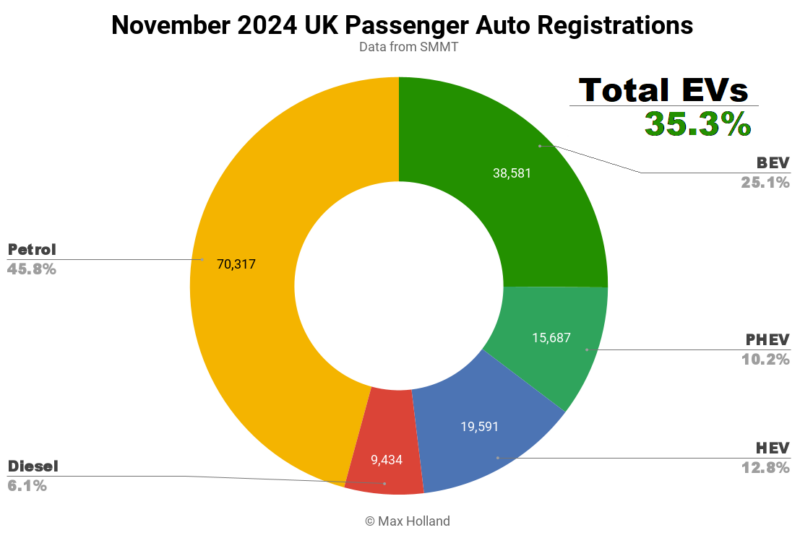

November noticed plugin EVs take 35.3% share of the UK auto market, up from 25.7% 12 months on 12 months. BEVs grew quantity by 58% YoY, and took 1 / 4 of the market, whereas PHEV quantity was flat. Total auto quantity was 153,610 items, down 2% YoY. Tesla was the main BEV model in November.

November’s gross sales figures noticed mixed plugin EVs take 35.3% share of the UK auto market, with full electrics (BEVs) taking 25.1%, and plugin hybrids (PHEVs) taking 10.2%. These examine with YoY shares of 25.7% mixed, 15.6% BEV, and 10.1% PHEV.

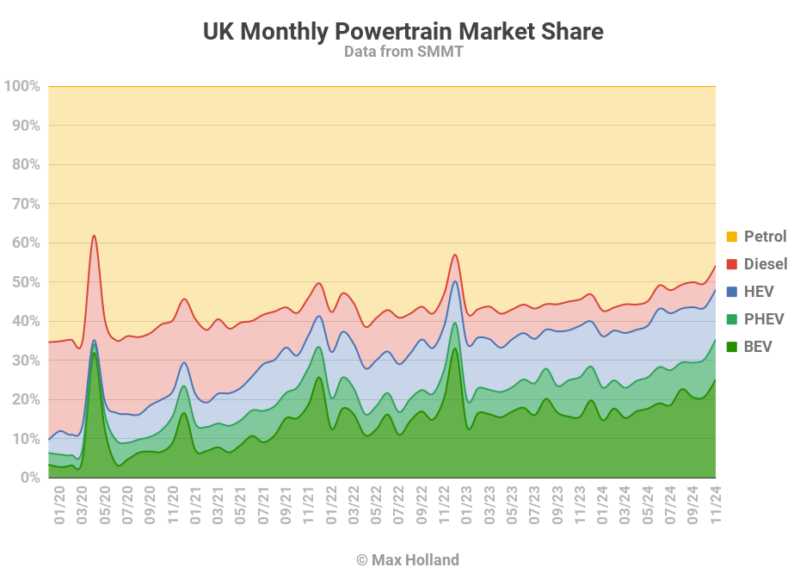

The normally sturdy development in BEV share comes as the tip of 12 months deadline for the 2024 ZEV mandate looms giant. Each producer should promote a sure minimal proportion of BEVs (and different low emissions automobiles), or commerce ZEV credit, to keep away from fines.

Whereas there’s a headline 22% goal, some wiggle-room for the primary 12 months of the system (with e.g. bonuses for enhancing emissions on non-BEV fashions bought), the efficient minimal goal for every producer’s BEV proportion of gross sales is in actual fact extra like ~19%.

This 19% continues to be a considerable elevating of the bar from 2023’s 16.5% full 12 months UK BEV share, as a result of this time it isn’t merely an trade common goal, as a substitute even the worst laggards have to fulfill this minimal bar (though some credit buying and selling between producers is allowed).

Underneath the scheme, legacy auto can not depart all of the heavy lifting to the likes of Tesla and MG, until they’re keen to pay out good cash to these opponents for ZEV credit. The wiggle room and work-arounds will steadily tighten within the coming years, even because the headline % targets themselves tighten – to twenty-eight% in 2025, 33% in 2026, then 38%, 52%, 66%, and 80% by 2030.

The legacy auto producers are at the moment lobbying the UK authorities exhausting to attempt to soften the ZEV targets, simply as they’re lobbying policymakers within the EU zone to loosen the emissions tightening guidelines for 2025 and past. Maybe they’re arguing that having “solely” proven their demonstration BEVs within the mid to late Nineteen Nineties, virtually 30 years has not been sufficient time for these corporations to learn to transition to cleaner know-how?

The place voiced by the UK trade consultant, the SMMT, makes no point out of the virtually 30 years of BEV foot dragging, squandered alternatives, and ICE rent-seeking, by legacy auto. The SMMT merely claims that: “Producers are investing at unprecedented ranges to convey new zero emission fashions to market and spending billions on compelling affords. Such incentives are unsustainable – trade can’t ship the UK’s world-leading ambitions alone.” (SMMT assertion).

Is anybody shopping for their spin?

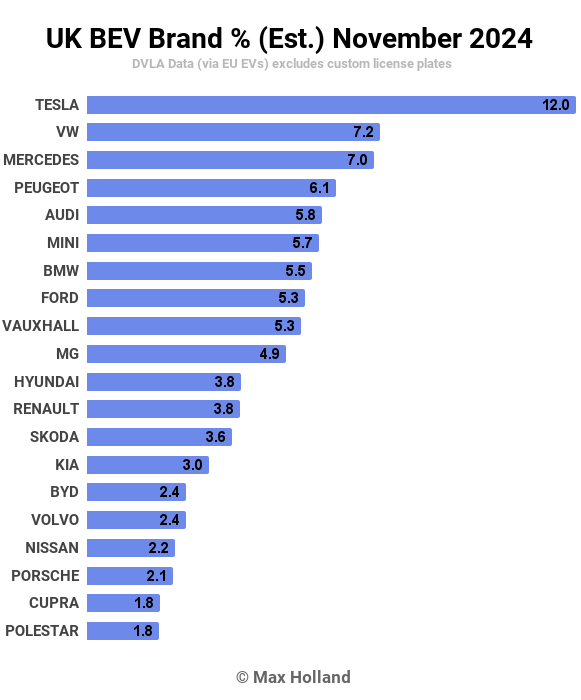

Finest Promoting BEV Manufacturers

Thanks largely to the persevering with recognition of the Mannequin Y, Tesla was as soon as once more one of the best promoting model for BEVs within the UK, with 12% of the general BEV market in November. This comes after a comparatively quiet month in October, when Tesla was taking a break following the standard September push.

In second place was Volkswagen model, with 7.2% of the BEV market, a giant step up from their share of simply 3.7% again in Q1 this 12 months. Simply behind, with 7.0% share, Mercedes took third spot.

The Volkswagen model has needed to step up in latest months – and can achieve this once more in December – as a result of that weak begin to 2024 means it’s the model with the most important unit shortfall in BEV gross sales, relative to the mandate (for extra see New Automotive’s evaluation).

This massive unit shortfall is partly as a result of Volkswagen is often the most important promoting automobile model within the UK (and thus all its unit numbers are large), and partly as a result of it’s nonetheless fairly some % under the ZEV goal. Volkswagen, nonetheless, is just not practically as far adrift in % phrases as a lot smaller manufacturers like Mazda and Suzuki, or medium-large manufacturers like Nissan and Ford.

Mini had a giant step up in BEV quantity in November, with over 2,000 items (round 4x its regular month-to-month quantity), taking 5.7% of the market. Evidently manufacturing of Mini’s new vary of BEV is now ramping up effectively.

Ford is one other model which continues to be adrift of the 2024 ZEV goal and having to step up its BEV gross sales. November noticed it promoting over 2,000 items (1.6x its latest month-to-month common quantity), nonetheless largely the brand new Explorer, and now supplemented by the just-launched Ford Capri, which bought over 250 items within the month.

The reasonably priced Dacia Spring continues to promote decently, including one other ~265 items in November.

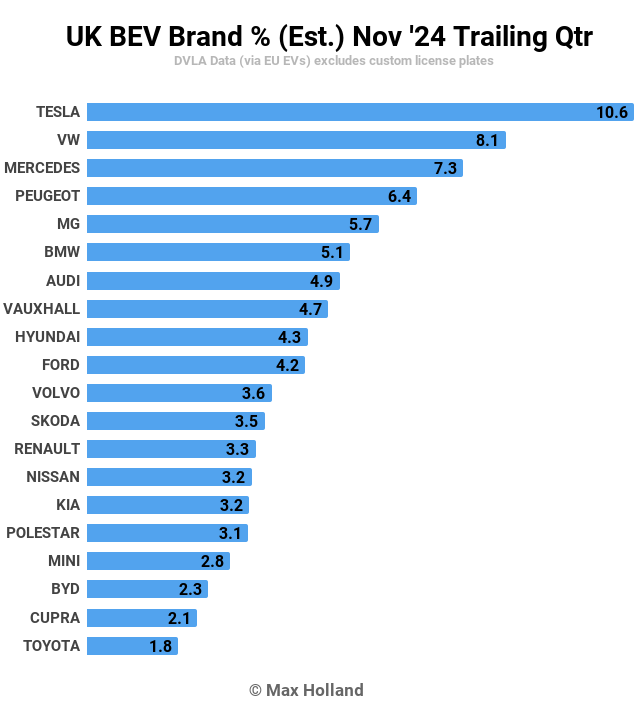

Let’s check out the 3-month rankings.

Tesla maintains its sturdy lead over the three month interval, with 10.6% of the UK BEV market, and over 13,000 gross sales.

Volkswagen has jumped up from third within the prior interval, to second by the tip of November, due to rising volumes dramatically over the previous three months. Previous to September its month-to-month common quantity was simply round 1,300 items, however since September its common has been over 3,300 items – some 2.5x larger.

Additional down the rankings we discover Ford now in tenth place, a great rise from its prior 18th place, and dashing to get near the ZEV mandate and keep away from paying out an excessive amount of cash for ZEV credit from its opponents!

Whereas the general UK auto market will doubtless meet the ZEV requirement for 2024 – and types will keep away from paying giant fines to the UK authorities – some model and manufacturing teams will exceed the targets and thus gather extra credit, and a few will miss and have to purchase these extra credit held by others, to make up for their very own shortfall. We’ll understand how issues work out — which manufacturers have been the winners and which have been the losers — by the point the mud settles in early 2025.

In the meantime, if in case you have been ready to get into a brand new BEV within the UK, it is a nice time to discover a low cost provide as some manufacturers (in quantity phrases, Volkswagen, Ford, Nissan, Renault) rush to get their BEVs out of the door. Don’t pay MSRP for any of the BEVs from these manufacturers in December.

Outlook

For November and December, the UK auto market is being steered by ZEV laws as a lot as by the broader financial local weather. The most recent GDP figures present YoY development of 1% in Q3 2024, an enchancment over the 0.7% of Q2. Inflation rose to 2.3 in October (newest knowledge), and rates of interest decreased to 4.75% in early November. Manufacturing PMI fell again to 48 factors in November, from 49.9 factors in October.

The ZEV mandate means we’ll see larger BEV share once more in December, presumably getting close to 30%, because the aforementioned manufacturers rush to push out extra quantity — even when they’ve to offer large reductions — to keep away from paying large transfers to their competitors (which is unquestionably extra painful than giving reductions to clients).

In case you’ve noticed nice bargains on new BEVs for UK shoppers, please do share them within the feedback in order that our readers can doubtlessly profit from some nice offers! What are your ideas on the UK auto market as we transfer in the direction of 2025? Will the legacy manufacturers reach pressuring the federal government to melt the mandate? Please bounce in to the feedback under and share your perspective.

Chip in just a few {dollars} a month to assist assist unbiased cleantech protection that helps to speed up the cleantech revolution!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

Join our day by day publication for 15 new cleantech tales a day. Or join our weekly one if day by day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage