Join every day information updates from CleanTechnica on e mail. Or comply with us on Google Information!

October’s auto market noticed plugin EVs take 30.2% share within the UK, up from 24.9% yr on yr. Each BEVs and PHEVs grew in quantity, while the general auto market shrank. Total auto quantity was 144,288 models, down 6% YoY, and barely beneath pre-2020 norms. The UK’s main BEV model in August was Volkswagen, with 9.6% share of the BEV market.

October’s gross sales totals noticed mixed plugin EVs take 30.2% share within the UK, with full electrics (BEVs) taking 20.7%, and plugin hybrids (PHEVs) taking 9.6%. These examine with YoY shares of 24.9% mixed, 15.6% BEV, and 9.3% PHEV.

With wholesome BEV share, and respectable efficiency of PHEVs, the UK’s mixed plugin share hit the very best degree seen since December 2022 (when Tesla made an unprecedentedly large push). That is excellent news and bodes properly for even increased floor in November and December (particularly because the deadline to fulfill the 22% ZEV mandate attracts close to).

Diesel share (together with MHEVs) has been weak, hovering simply over 6% (on common) for the previous 7 months, with solely diminishing prospects for the longer term. 12 months to this point diesel share is at 6.4%, in comparison with 7.6% at this level final yr. Share is trending to hit 3% round 4 years from now.

Not like Norway, the place diesel gross sales proceed to persist at a really low degree, due issues in regards to the harsh northern situations, the UK has no excessive use circumstances that time to diesel because the routine reply. With battery know-how additional advancing over the following few years, BEVs — or a minimum of PHEVs and EREVs — will doubtless reliably deal with any sensible driving activity within the UK.

Petrol share (together with MHEVs) is coming perilously near dipping beneath the 50% mark on a everlasting foundation. The previous 5 months have seen a mean of fifty.7% share, and slowly trending down. We are able to count on this to dip beneath 50% within the subsequent two months, maybe quickly get better in H1 2025, and keep beneath 50% thereafter.

By this level subsequent yr, mixed petrol and diesel will doubtless be dipping beneath 50% for the primary time.

Main BEV Manufacturers

After Tesla’s massive push in September, the model took a again seat in October, permitting Volkswagen to take the highest spot, with 9.6% share of the UK BEV market.

In second place was Mercedes, with 8.2% share, simply forward of Peugeot, with 8.1% share.

It is a document efficiency for Peugeot, its first ever time within the UK’s prime 3 spots. Clearly Tesla’s October absence helps, however Peugeot has anyway just lately been performing strongly, taking seventh in July, 4th in August, and fifth in September. Let’s see if this may be sustained over an extended interval.

Skoda additionally had a comparatively sturdy month, with the Skoda Enyaq reportedly taking the highest BEV mannequin spot with someplace over 1450 models. With nonetheless just one BEV mannequin on sale, Skoda should now carry their subsequent BEV to market, and the corporate plans to take action with the Elroq (a Niro-sized SUV) someday early in 2025. It’s already being fanfared on Skoda’s UK web site.

We are able to’t learn an excessive amount of into anyone month’s leads to the UK, attributable to being a batch-supplied right-hand-drive market, with essentially erratic month-to-month mannequin and model volumes.

One or two knowledge factors stand out as value highlighting. The Dacia Spring lastly noticed respectable quantity within the UK, with over 328 models registered, from simply 4 preliminary models in September. This comes 4 years after the Spring went on sale in neighbouring France!

The Spring’s UK MSRP begins from £14,995, however offers may be discovered nearer to £14,000. The Spring comes with a 3 yr 60,000 miles normal automobile guarantee, which may be inexpensively prolonged to 7 years if official servicing intervals are adhered to. For these eager to personal a recent new BEV, with an extended guarantee, and don’t must do common lengthy journeys within the automobile, the Spring is as inexpensive because it will get within the UK.

The MG Cyberster, which debuted final month with round 70 models, added one other ~90 models in October. That is nice quantity for a distinct segment 2 seat sports activities automotive, let’s see the way it continues.

Speaking about sturdy volumes, the brand new Porsche Macan grew shortly from its September debut (~113 models), including a minimum of ~460 extra models in October. This doubtless places it in or near the highest 20 greatest promoting BEVs within the UK (although we don’t have sturdy sufficient mannequin knowledge to know for certain).

Chery launched the Omoda E5 SUV (the BEV model of the C5) in September with 187 models, and added one other ~220 models in October. With no devoted supplier community, the Omoda is being distributed and serviced although unbiased UK retail community, Arnold Clark.

The Omoda E5 is Kia Niro sized (4,424 mm), with a reasonably respectable WLTP vary of 257 miles, and okay (not nice) DC quick charging (10% to 80% in round 40 minutes). It’s priced from £33,000 MSRP, and comes with an extended 7 yr guarantee. Pre-registered offers may be discovered for round £30,000. The problem is that Kia Niro offers may be discovered from £32,000, with longer vary (285 miles WLTP), from a better-known model. Alternatively, the Omoda battery is LFP chemistry from BYD, which must be thought of an enormous plus level, with over 3,000 cycles, for 20+ yr longevity.

The brand new Ford Capri debuted within the UK in October, with round 44 models. For an outline of this new mannequin from Ford, test my latest Norway report. Lastly, the Xpeng G6 additionally broke the ice within the UK in October, although with simply 5 preliminary models, which can be for check drives (and suggestions) reasonably than buyer deliveries. Let’s regulate it.

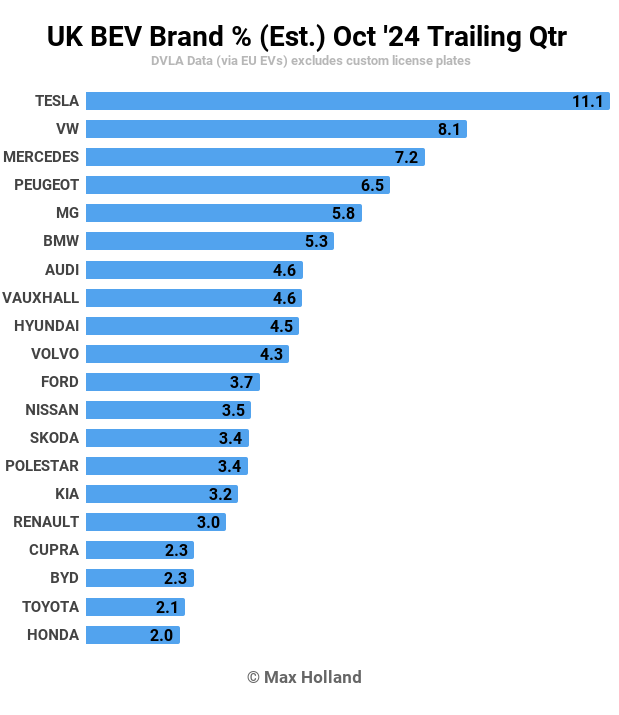

Right here’s the trailing-Q chart:

As regular, Tesla may be very dominant, with a good hole separating it from runner-up Volkswagen model (8.1%). Mercedes is in third with 7.2%.

Many of the strikes because the prior interval are modest, with essentially the most notable slides being from BMW, Audi, Volvo, Kia, and BYD, every stepping again 3 or 4 spots.

The largest climbers are Peugeot and Ford. Within the DVLA knowledge that we’ve entry to, Peugeot’s gentle vans (Accomplice and Knowledgeable, sometimes for final mile deliveries, or minicabs) are included within the model totals. Since these vans are comparatively fashionable, this juices Peugeot’s UK numbers significantly, a lot moreso than different manufacturers, so simply concentrate on that twist within the knowledge supply. Nonetheless, even with out the vans Peugeot would nonetheless be doing pretty properly, although maybe in seventh or eighth, reasonably than third or 4th. Both approach you take a look at it, Peugeot has climbed 5 or 6 spots because the prior interval, an excellent enchancment.

Ford has climbed a powerful 11 spots, from 18th to seventh, largely because of the success of the brand new Explorer, which is now being joined by the brand new Capri. It is a massive flip round from their earlier lacklustre BEV picture of just some months in the past. Ford’s totals are additionally barely juiced by the inclusion of their Transit van, however to a a lot lesser diploma than Peugeot’s. As soon as the Capri will get rocking, how far will Ford climb – can it get close to the highest 5?

Regardless of offering welcome new additions to the BEV fashions out there, there’s little prospect of Dacia or Omoda getting into the highest 20 anytime quickly (however I might be very completely happy for Dacia to show me fallacious)! Against this, with the rising recognition of the brand new Macan, there’s each prospect of Porsche getting into the chart subsequent month, so let’s look out for that.

Outlook

Though October noticed total auto quantity barely down from a yr in the past, the UK’s year-to-date auto market has grown 3.3% from this level in 2023, and can find yourself near 2 million models. It is a bit down from the two.3 million seen in among the good years of the 20 years pre-2020, however nonetheless barely above the 1.94 million models of 2011 (the weakest yr of that interval).

With the pandemic now not being a good clarification for the persevering with weak spot (if something we must be seeing a rebound), we’ve to look to the broader financial system. Though higher than some neighbouring nations, and step by step assuaging, the UK’s newest knowledge on the trailing 12 months of quarterly YoY GDP figures aren’t nice (+0.3%, – 0.3%, +0.3%, +0.7%). Q3 2024 is just not but in, however is anticipated to be roughly +0.6%, earlier than additional modest enhancements subsequent yr. Inflation shifted decrease (1.7%), as did rates of interest (4.75%), although manufacturing PMI declined to 49.9 factors in October, from 51.1 factors prior.

Clearly a weak-ish auto market might be considered a constructive while ICE powertrains are nonetheless dominating gross sales. Alternatively, a stronger UK financial system would doubtless increase the velocity of the EV transition – with extra public funds for infrastructure, and extra client spending energy to stretch to still-relatively-expensive BEVs.

The one strong signpost is the UK’s ZEV mandate which is now set in stone, and requires producers to make 22% BEV gross sales this yr (with some wiggle-room), 28% subsequent yr, and rising thereafter. There’s no prospect of a re-negotiation of this, and so the (largely legacy) business foyer, the SMMT remains to be in search of monetary help to attain it, saying:

“Transferring the market quickly in the direction of these bold targets wants daring and compelling incentives for shoppers. Producers are presently shoring up demand with historic ranges of help, however that is unsustainable in the long run because it threatens [profits] viability. With out the federal government help to match the producers’ dedication, there should be an pressing evaluate of the market’s efficiency and the regulatory mechanisms driving the transition.” (SMMT assertion)

What the assertion conceals are the document income, administration bonuses, CEO salaries, and shareholder payouts that many legacy producers paid to themselves in 2022 and 2023. Realizing that we’re in the course of a difficult know-how transition (although one stuffed with alternatives), why didn’t these producers as a substitute plough revenues again into investments in price reductions and scale-ups for BEV applied sciences? Now they arrive asking for incentives? The identical outdated angle of entitlement appears to be in impact.

What are your ideas on the UK’s auto market and transition to EVs? Which of the brand new fashions are you enthusiastic about, or maybe planning to check out? Please be a part of within the dialog within the feedback beneath.

Chip in a number of {dollars} a month to assist help unbiased cleantech protection that helps to speed up the cleantech revolution!

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day e-newsletter for 15 new cleantech tales a day. Or join our weekly one if every day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage