Join day by day information updates from CleanTechnica on e mail. Or observe us on Google Information!

T&E analyses the methods that producers are anticipated to make use of to conform.

Abstract

The EU’s 2025 Automotive CO2 goal is reachable and possible

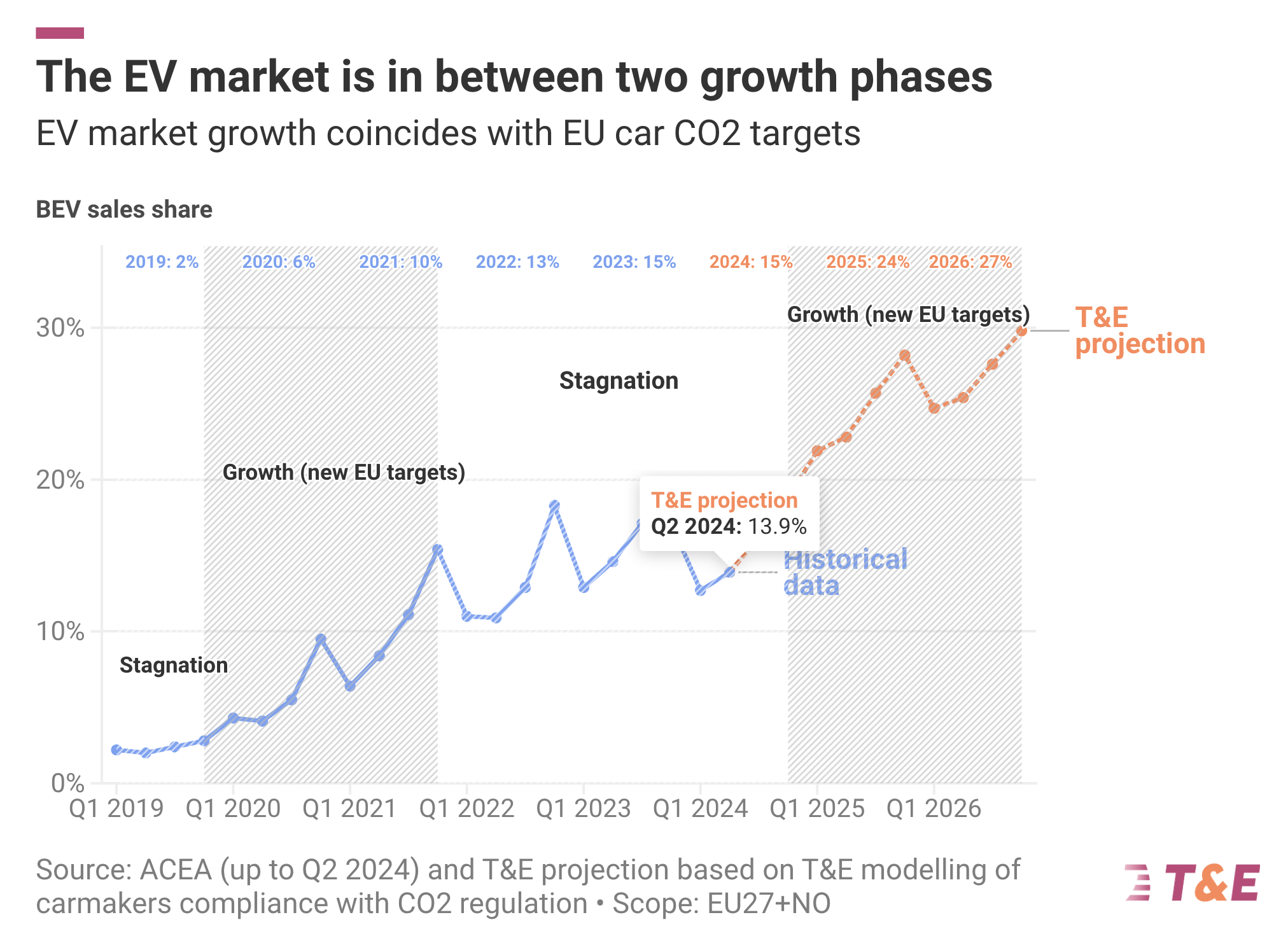

After years of stagnant EV gross sales as a result of lack of recent automotive CO₂ targets, carmakers will face stricter requirements in 2025, following the final targets set in 2021. Whereas some carmakers have been calling to weaken the regulation, T&E exhibits that each one carmakers can meet their 2025 targets. T&E breaks down the methods carmakers are anticipated to make use of to conform based mostly on modelling of compliance situations counting on: gross sales knowledge, carmakers’ public plans, and evaluation of knowledge from market analysis firm GlobalData. The compliance choices embody growing gross sales of full electrical automobiles (BEVs), gentle and full hybrids (HEVs) and plug-in hybrids (PHEVs), in addition to numerous compliance flexibilities. This evaluation supplies an perception into carmakers’ paths to adjust to the goal in 2025.

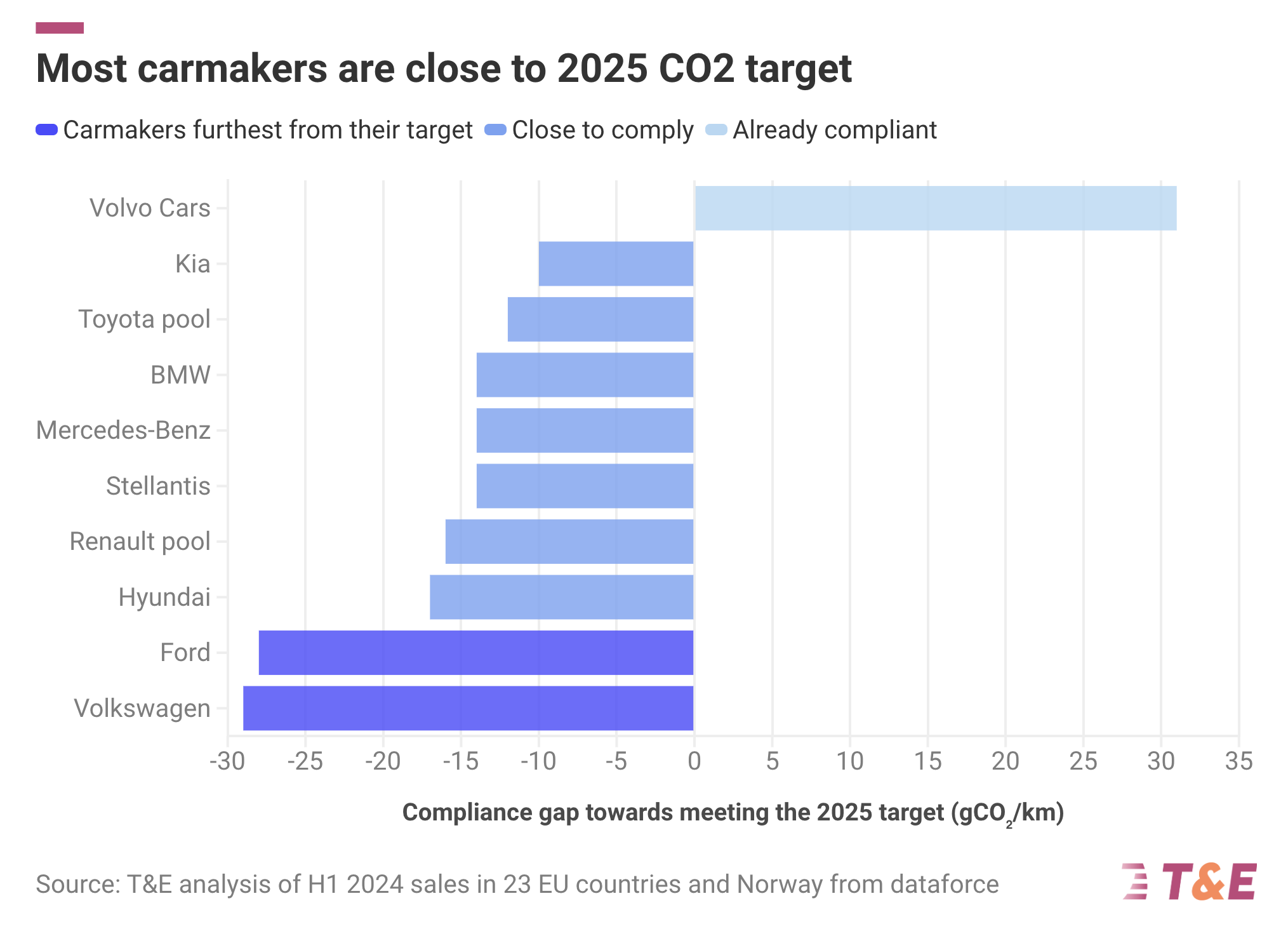

As with previous automotive CO₂ targets, carmakers are anticipated to shut their compliance hole within the goal 12 months, reasonably than forward of time. Between 2019 and 2020, carmakers furthest away from their targets improved their CO₂ efficiency by 20 gCO₂/km. Within the first half of 2024, most carmakers are near assembly their goal with gaps starting from 10-17 gCO₂/km. Leaders in EV gross sales resembling Volvo Automobiles have already reached their 2025 goal. Volkswagen (VW) and Ford are the furthest behind with gaps of 28-29 gCO₂/km and will contemplate forming compliance swimming pools with leaders to cut back the hole. As an illustration, if VW swimming pools with Tesla, it might solely want to attain a 17% BEV share in 2025 (down from 22%). Equally, if Ford swimming pools with Volvo once more, BEVs would wish to account for simply 9% of its gross sales, as a substitute of 21%.

It’s essential to emphasize that the 2025 goal is not an electrical automotive mandate, and — technically — no necessary EV gross sales share is critical. The goal, proposed again in 2017 and unchanged since then, is a CO₂ common: promoting extra environment friendly petrol automobiles (or fewer SUVs) helps as a lot as promoting electrics. As well as, quite a few flexibilities are allowed: a further bonus for >25% ZLEV gross sales, eco improvements, in addition to pooling emissions with different producers, e.g. pure EV gamers.

In 2025, carmakers are anticipated to spice up EV gross sales in 2025. In T&E’s central compliance situation, EV gross sales are anticipated to rise to 24% market share in 2025 (from 14% within the first half of 2024), supported by an growth of mass market EV choices, together with seven inexpensive (<€25,000) EVs accessible. If carmakers rely extra on hybrids, they would wish much less BEVs to conform (20%). The expansion in EV gross sales would account for greater than half (60%) of the CO₂ discount wanted to achieve 2025. This comes after three years of stagnation, as a result of carmakers deal with income from ICE and higher-priced EVs.

Whereas BEVs play the most important position, carmakers additionally depend on different compliance choices. In T&E’s compliance situation, on common, 20% of the CO₂ discount can be achieved by promoting extra hybrids, whereas regulatory flexibilities would contribute to a 12% CO₂ discount, and PHEVs may present 8% of the enhancements. Stellantis (33%) and VW (30%) would rely probably the most on HEV gross sales to fulfill their targets. Consequently, regardless of not being a future proof possibility, the share of gentle hybrids is predicted to double (from 19% to 37%). BMW is predicted to rely most on PHEVs (18%).

The automotive CO₂ regulation has confirmed efficient and can proceed to push carmakers in direction of electrification however must be accompanied by nationwide EV insurance policies: charging masterplans and secure, focused subsidy schemes. To make sure Europe’s automotive business stays aggressive and leads within the mass-market EV sector, policymakers should resist calls to weaken the 2025-2035 targets or delay compliance. The present lead loved by Chinese language EV makers solely exhibits that the longer the EU protects its laggard automakers, the much less aggressive they are going to be.

Half 1

Stagnation and progress: how the European EV market works

The BEV share of the European automotive market decreased barely to 13.3% within the first half of 2024, in comparison with 13.8% within the first half of 2023 and 15.4% for the entire of 2023.

Stagnation section: The gradual progress of BEVs within the 2022-2024 interval is as a result of CO₂ requirements design and carmakers revenue pushed technique. This stagnation has been anticipated by T&E and market analysts since 2020.

-

The EU automotive CO₂ regulation is designed with 5-year steps with new targets in 2025 and 2030. Previous proof exhibits that carmakers don’t adjust to automotive CO₂ targets upfront, however solely when the targets require it. Earlier T&E evaluation confirmed carmakers have been solely half-way to the 2020 goal 4 months earlier than the beginning of 2020.

-

Carmakers deal with ICE income forward of the subsequent progress section pushed by 2025 targets. Within the stagnation section, carmakers prioritise short-term income by way of the sale of high-margin automobiles (e.g. Volkswagen’s “worth over quantity” technique). Earlier T&E evaluation has proven that carmakers’ disproportionate deal with bigger, extra premium fashions has resulted in excessive costs for EVs in Europe which has slowed down EV gross sales because of this.

Development section: Carmakers are anticipated to ramp up mass-market inexpensive EVs to fulfill 2025 targets

Within the subsequent progress section from 2025 onwards, electrical automotive gross sales would choose up as carmakers must prioritise EV gross sales to fulfill the subsequent automotive CO₂ goal. As introduced in part 4, T&E expects EV gross sales to develop to twenty%-24% in 2025, partly because of inexpensive fashions coming to the market (see part 3). This stop-and-go technique creates a succession of stagnation and progress phases.

Nonetheless, as carmakers prioritise their income and shareholder payouts, many OEMs are calling on the European Fee to weaken the automotive CO₂ regulation even supposing the targets have first been proposed again in 2017. As an illustration, ACEA’s president Luca De Meo is asking for “a bit of extra flexibility” within the regulation implementation whereas Volkswagen needs the EU to melt CO₂ emissions targets. This briefing appears to be like forward to 2025, analysing carmakers’ compliance hole based mostly on gross sales within the first half of 2024 and describing how all carmakers can adapt their gross sales to fulfill the targets (methodology described in annex 6.1 of downloadable pdf briefing).

Half 2

Carmakers’ progress in direction of 2025 CO₂ targets is uneven

Whereas Volvo Automobiles is already on monitor to fulfill its 2025 goal based mostly on gross sales within the first half of 2024, Volkswagen and Ford are furthest away. Different carmakers are within the center and anticipated to fulfill their targets. This general compliance image with one chief, two laggards and different carmakers with a reasonable hole round 10 gCO₂/km has not modified a lot since 2023. Nonetheless, given there’s been a BEV slowdown since 2023, the compliance hole has barely elevated for many carmakers over the primary half of 2024 (in comparison with the complete 12 months 2023). This case shouldn’t be new as most carmakers had related gaps with their 2020 goal in 2019.

The BEV slow-down within the first half of 2024 led common CO₂ emissions to extend to 109 gCO₂/km from 107 gCO₂/km in 2023. Volvo Automobiles is the one legacy carmaker that’s already compliant (over-compliance of 31 gCO₂/km). Among the many non-compliant carmakers, Kia is the closest to the 2025 goal with a niche of 10 gCO₂/km. A lot of the carmakers’ targets are effectively inside attain with gaps starting from 10 and 17 gCO₂/km.

To shut the hole by 2025, Ford and Volkswagen might want to redouble their efforts.

Ford and Volkswagen are the furthest away from their targets with gaps of 28 and 29 gCO₂/km respectively. Whereas these two carmakers might want to double down on their efforts in 2025 to shut the hole, they’ve many doable compliance methods as highlighted in part 4.

Again in 2019, carmakers additionally had massive gaps with their 2020 targets.

Trying on the market common, the compliance hole is 15 gCO₂/km in H1 2024, the same worth because the 13 gCO₂/km hole in 2019 in comparison with the 2020 goal. BEV gross sales are anticipated to normalise within the second a part of 2024 because the market recovers from the abrupt removing of the subsidy in Germany (e.g. by decreasing EV costs as VW has already carried out). The complete 12 months 2024 hole can be decrease than the present 15 gCO₂/km and will even grow to be decrease than 2019. Hyundai was the foremost carmaker that was the furthest away from its 2020 goal in 2019 with a niche of 17 gCO₂/km. Regardless of this hole, it nonetheless over-complied in 2020, bettering its CO₂ efficiency by 20 gCO₂/km. Ford and Volkswagen at the moment have considerably larger gaps than in 2019 (Ford finally shaped a pool with Volvo Automobiles and VW with MG) whereas Kia and Mercedes-Benz are at the moment doing higher than 5 years in the past.

Learn Half 3 of the report, “Carmakers methods to adjust to their CO₂ targets in 2025,” Half 4, “EV gross sales to develop as carmakers deal with compliance,” and extra within the full report right here.

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

Newest CleanTechnica.TV Movies

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage